Presented by LaSalle Mortgage

This report exists because there is a growing gap between how the real estate market is often described and how it is actually experienced. National headlines rely on broad narratives. Those narratives are useful at a distance but they flatten what is, in reality, a deeply local industry. In the Inner East Bay, conditions can change meaningfully from one neighborhood to the next. Sometimes from one block to the next. When everything gets summarized into a single story, important details get lost. To understand what really happened in 2025, we went directly to the agents doing the work.

WHY THESE AGENTS MATTER:

These are not observers. They are participants. Collectively, they were involved in more than 2,500 transactions during the survey period. They negotiate offers. They manage client expectations. They see how deals start, how they stall, how they get renegotiated and how clients actually make decisions when real money is on the line.

66 Top Agents

Top producing real estate agents across the Inner East Bay, selected by closed sales volume.

This report draws on perspectives from 66 of the top 100 agents in the Inner East Bay, ranked by closed sales volume in BridgeMLS from January through September 2025. The geography spans Alameda, Albany, Berkeley, El Cerrito, Kensington, Oakland, Piedmont, Richmond and San Leandro.

2500+ TRANSACTIONS IN 2025

Collective deal experience across listings, buyers, negotiations, and fall-throughs.

WHAT THIS REPORT IS NOT:

This is not a forecast. It is not market advice. It is not advocacy for buying, selling or waiting. The goal is documentation, not persuasion. We are reporting what experienced practitioners saw, said and did during a year that did not fit clean narratives.

HOW TO READ THIS:

Treat this as a snapshot. The insights are qualitative and grounded in lived experience, not statistical modeling. In some areas, you will see consensus. In others, sharp disagreement. That split is intentional. It reflects a market that resists tidy explanations.

This report was compiled by LaSalle Mortgage, a locally based lender working across brokerages throughout the Inner East Bay. That positioning gave us access to agents across firms and the ability to collect perspectives that do not usually get aggregated in one place.

We are offering this as a practical reference for understanding how the Inner East Bay market actually functioned in 2025 and how experienced agents are thinking about what comes next.

– Brady Thomas

Branch Manager

LaSalle Mortgage

The Inner East Bay real estate market in 2025 did not follow a single storyline. National narratives suggested a slowdown driven primarily by interest rates. What agents experienced on the ground was more nuanced. Activity persisted, but the market became far more selective. Outcomes depended heavily on neighborhood, price range, property condition and timing. Broad assumptions were unreliable. Precision mattered.

89% of Agents described the 2025 marked as Strong or Balanced

A MARKET THAT PUNISHED ASSUMPTIONS:

What worked in prior years didn’t reliably get the job done in 2025. Buyers and sellers who relied on generalizations often struggled to gain traction. Agents repeatedly emphasized that success came from understanding micro-markets and acting decisively within them. Homes that were well-priced and well-positioned continued to move quickly. Nearly three-quarters of agents reported that the majority of their listings sold above asking price, though overbids were more modest than during peak years.

Even when homes sold above the asking price, appraisals rarely became a problem. In most cases, the value confirmed during the lending process matched the agreed-upon price, allowing deals to move forward without disruption. While appraisal issues were rare, insurance emerged as a new challenge. Agents reported broad concern around rising insurance costs and coverage availability, particularly for homes in higher fire-risk areas or with older electrical systems. In some cases, insurance uncertainty became a deciding factor for buyers, introducing a new friction point that felt distinctly regional.

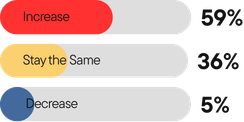

59% of Agents expect inventory to increase in 2026

EXPECTATIONS (NOT RATES) CREATED FRICTION:

One of the clearest themes in the report was the role of expectations. Buyer hesitation was driven more by uncertainty around timing, politics and the job market than by interest rates themselves. Many buyers had acclimated to higher rates but remained unsure about when to act. Sellers, in many cases, remained anchored to peak conditions from earlier cycles. Much of the work agents did in 2025 involved resetting reference points and helping clients navigate a market that no longer behaved uniformly.

91% of Agents said fewer than 1 in 5 buyers used seller credits or creative financing

WHY SIMPLIFIED NARRATIVES FELL SHORT:

Several agents pointed to clear divergence across the Inner East Bay. Markets such as Berkeley, El Cerrito and Albany continued to see intense competition and price strength, while parts of Oakland experienced softer demand and increased buyer hesitation tied to local conditions and services. This fragmentation helps explain why simplified narratives failed to capture what was actually happening on the ground.

This report is not a forecast and it is not a call to action. It does not attempt to predict prices, interest rates or market direction. The insights are qualitative and drawn from firsthand experience. They are intended to document how the Inner East Bay market functioned in 2025 and where assumptions deserve closer scrutiny.

This report is based on input from real estate agents identified as the top 100 agents by closed sales volume in the Inner East Bay, using BridgeMLS data from January 1 through September 30, 2025. Rankings were based on closed residential transactions across all property types within the defined geography.

9 INNER EAST BAY CITIES COVERED

Alameda, Albany, Berkeley, El Cerrito, Kensington, Oakland, Piedmont, Richmond and San Leandro

HOW AGENTS WERE IDENTIFIED:

The intent was to capture perspectives from the most active agents operating in the Inner East Bay during 2025, regardless of brokerage affiliation or geographic focus within the region.

The designation “Top 100” reflects ranking by transaction volume within this dataset (BridgeMLS from January to September 2025). It is a selection framework, not a claim of exclusivity or endorsement.

OUTREACH AND PARTICIPATION:

Agents who met the qualification criteria and could be identified through available MLS data were invited to participate. Outreach included direct emails, text messages and phone calls.

Participation was voluntary. Of the 100 agents identified, 66 completed the survey. Some qualifying agents do not appear due to non-response, outdated contact information or timing constraints. In some cases, invitations may not have been received. Any omissions were unintentional and should not be interpreted as exclusion.

DATA COLLECTION:

Participating agents completed an online survey consisting of 14 quantitative multiple-choice questions and 11 qualitative open-ended questions.

The quantitative results are summarized in the “Market by Numbers” section of the report. The qualitative responses form the foundation of the narrative sections and are quoted directly where permission was granted.

INTERPRETATION AND ANALYSIS:

Qualitative responses were reviewed in full and analyzed by LaSalle Mortgage. Common themes were identified, grouped and synthesized across responses. Where helpful, the frequency of similar viewpoints is noted to provide context.

LIMITATIONS:

This report reflects a snapshot in time and is based on survey responses, rather than real-time transaction data. Not every participant answered every question and response depth varied. While care was taken to identify and contact qualifying agents, it is possible that some qualifying agents were not reached.

The findings represent a good-faith effort to document and synthesize perspectives from highly active agents operating in the Inner East Bay during the period studied.

2025 East Bay Market Mood: How would you describe the East Bay market in 2025?

11% SLUGGISH

44% BALANCED

42% STRONG

3% RED HOT

Do you expect prices to rise, fall or stay flat in 2026?

61% RISE

29% FALL

10% STAY FLAT

Were buyers more confident in 2025 than 2024?

41% More Confident

38% About the Same

21% Less Confident

Do you expect inventory levels to increase in 2026?

59% INCREASE

36% STAY THE SAME

5% DECREASE

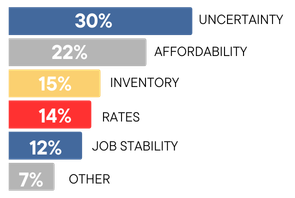

The Pause Button: What’s the #1 reason that buyer’s are hesitating today?

30% UNCERTAINTY

22% AFFORADABILITY

15% INVENTORY

14% RATES

12% JOB STABILITY

7% OTHER

Were low appraisals more of an issue than in previous years?

66% NO

24% ABOUT THE SAME

7% YES

2% NOT SURE

Are sellers holding back from listing homes due to interest rates?

52% YES

39% NO

9% NOT SURE

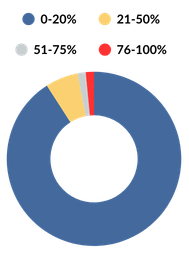

What % of your buyers negotiated seller credits in 2025?

90.9% Reported 0-20%

6.1% Reported 21-50%

1.5% Reported 51-75%

1.5% Reported 76-100%

91% of agents reported 0-20% of their buyers used seller credits

91% of agents reported 0-20% of their buyers used seller credits

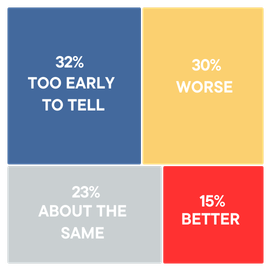

Will 2026 be better or worse for buyers?

32% TOO EARLY TO TELL

30% WORSE

23% ABOUT THE SAME

15% BETTER

What price range was the most competitive in 2025?

2% UNDER $1M

53% $1M-$1.5M

31% $1.5-$2M

14% $2M+

2% NO ANSWER

What % of your 2025 listing sold over the asking price?

74% of agents answered that more than 75% of their listings sold over asking price

4 Reported 0-25%

3 Reported 26-50%

10 Reported 51-75%

48 Reported 76-100%

Who do you believe will have more leverage in 2026?

19% BUYERS

51% SELLERS

30% BALANCED

Were you heavier on listings or buyers in 2025?

61% LISTINGS

31% BALANCED

8% BUYERS

What was the biggest shift in the East Bay market this year?

Agents described 2025 as a market defined by separation and selectivity.

Agents consistently described the biggest change in 2025 as the loss of a single, predictable market. Results varied widely by neighborhood, price range and type of home (sometimes within the same city). Berkeley, El Cerrito and Albany were often competitive and active, while parts of Oakland saw slower demand and more cautious buyers. The pace of the market also shifted. Instead of moving in a steady seasonal pattern, activity came in waves. Quiet stretches were followed by sudden bursts of competition. Timing mattered more than usual. Several agents noted that homes listed earlier in the year often performed better than similar homes listed later. In some areas, buyers gained limited leverage over sellers due to lack of activity. This was not widespread, but it showed up in specific neighborhoods and price points. Pricing and preparation became critical. Homes that were priced well and ready to move into sold quickly. Others lingered, even nearby. Uncertainty also played a role. Economic concerns, politics and changes in tech-related wealth influenced buyer behavior. Insurance became a new challenge as well. Higher costs and limited coverage, especially in fire-risk areas, affected buyer decisions in ways agents had not seen in prior years. Taken together, agents did not describe 2025 as a simple slowdown. They described a market that became more fragmented, more timing-sensitive and more dependent on micro-market dynamics than in recent memory.

36% Increased market fragmentation and volatility

Agents describe uneven conditions across cities, price bands, and timeframes.

25% Temporary buyer leverage in specific segments

Buyers gained leverage briefly, especially early in the year or in weaker submarkets.

22% Inventory increases changing negotiation dynamics

Higher inventory affected leverage without creating broad softness

17% Oakland-specific softness vs nearby strength

Oakland, particularly under $1M, softened more than adjacent cities.

“With the market missing the move-up seller/buyer, we have a mismatch between what is available to buy (inventory) and what buyers want (demand). We have a buyer pool who is heavily seeking well-maintained, high-quality smaller homes.”

Alissa Custer, DISTRICT HOMES

“Buyers are much picky about the condition of the due to the interest rates rising and uncertainty in the economy.”

Kara Thacker, THE AGENCY

“The insurance concern took on a heightened dimension. I witnessed a buyer pull out of contract based on fear of the general future of insurance in the state.”

Martha Hill, VANGUARD PROPERTIES

“The biggest shift was the market drawing a very clear line between A+ quality/location and everything else.”

Roxanna Ahlbach, RED OAK REALTY

FIELD INSIGHT: The biggest shift was not weaker demand overall…but demand becoming far more selective and sensitive to timing and micro-market conditions.

What do buyers consistently misunderstand?

Agents shared where buyers’ expectations most often diverge from on-the-ground market realities.

Agents consistently said buyers misunderstood how pricing and competition actually work. Many treated the list price as a signal of value, when in practice it was often a starting point designed to attract interest. Buyers also tended to assume the market was uniformly in their favor, missing the reality that many neighborhoods and price ranges remained highly competitive. Several agents noted that buyers overestimated their negotiating power. Some believed patience alone would lead to better deals, without realizing that waiting often meant missing specific homes rather than gaining leverage. Buyers frequently assumed better options would appear automatically, when in reality the right homes often came and went quickly. Another common misunderstanding involved risk and certainty. Buyers often focused heavily on price while underestimating how much sellers value clean, reliable offers. Agents repeatedly pointed out that strong financing, fewer contingencies and clarity around closing still mattered, even when competition appeared lighter. There was also confusion around overbidding. Buyers sometimes viewed offers above asking as irrational, rather than recognizing that limited inventory and concentrated demand pushed prices higher in certain segments. Importantly, agents did not describe buyers as uninformed. Instead, buyers were often anchored to outdated expectations or national headlines. Much of an agent’s role in 2025 involved resetting assumptions, managing fatigue and helping buyers understand how this market actually rewarded preparation and decisiveness.

42% List price mistaken for true value

Buyers assume list price reflects market value rather than pricing strategy.

33% Buyer leverage overestimated

Buyers believe conditions broadly favor them when leverage is highly situational.

24% Overbidding dynamics misunderstood

Overbidding is seen as optional or irrational instead of context-dependent.

18% Waiting viewed as a viable strategy

Buyers expect patience alone to improve outcomes.

“Prices are not going down for the homes that are in good condition, have a great location and lot and layout are ideal.”

Teresa Baum, COMPASS REAL ESTATE

“Buyers don’t understand that the listing price is not necessarily the seller’s expectation or where the property is likely to sell.”

Pamela Strike Fullerton, THE GRUBB CO

“I believe many buyers misunderstand comparables and value (and I think quite a few agents misinterpret them, as well). There is a common misconception that if no competing offer appears, the value of a property suddenly drops by hundreds of thousands of dollars.”

Allie Pembleton, KELLER WILLIAMS

“I wish we would all price things more realistically. It would save a lot of time and heartache.”

Andrea Gordon, COMPASS REAL ESTATE

FIELD INSIGHT: Buyer hesitation seems to be less about interest rates and more about misreading how pricing, leverage, and competition actually work in today’s market.

What are sellers not grasping about the market?

Agents described where sellers most often clash with current buyer behavior and market dynamics.

One of the clearest patterns was a gap between seller expectations and current market reality. Pricing was the most common issue. Many sellers referenced peak sales or assumed strong demand would overcome ambitious pricing, even when early feedback suggested otherwise. Sellers also underestimated how selective buyers had become. Inspection issues, deferred maintenance and insurance concerns carried more weight than many expected. Move-in-ready homes continued to attract strong interest, while properties needing work faced sharper discounts or longer time on market. Several agents noted that sellers were surprised by buyers’ willingness to walk away. Many expected buyers to push through issues or renegotiate later, only to see deals cancelled when terms did not align. Timing emerged as critical. Sellers often believed the right buyer would eventually appear, overlooking how much leverage shifts after the first few weeks. Once early momentum faded, buyers gained more control and sellers had fewer options. Geography added another layer of confusion. Sellers frequently assumed strength based on a nearby neighborhood or even a nearby block, without recognizing how micro-location affected outcomes. Agents also described an emotional component. Some sellers took market feedback personally and resisted adjustments even when data was clear. This resistance explains why resetting expectations required more effort in 2025 than in prior years.

44% — Pricing expectations anchored to prior peaks

Sellers rely on outdated comps or peak-market assumptions.

36% — Buyer selectivity underestimated

Buyers are far more critical of condition, inspections, and risk.

27% — Turnkey condition matters more than expected

Homes needing work face steeper discounts and slower demand.

19% — Overconfidence in waiting out the market

Sellers believe patience will produce better offers.

“Insurance has become a complicated topic for sellers. Many don’t fully grasp the challenges buyers face just to secure coverage.”

Claudia Mills, KELLER WILLIAMS

“While this does not apply to every Seller, there is a consistent pattern of slower acceptance of actual market value, which can influence the initial list price and the willingness to accept an offer at the deadline.”

Gillian Leslie, RED OAK REALTY <img=gillianleslie>

“In today’s market, buyers will absolutely pay a premium for a home that is turnkey but that means investing upfront to fix flaws and make the property feel picture perfect.”

Adrienne Krumins & Anian Tunney, THE GRUBB CO.

“The same aspects of their house that gave sellers “pause” when they bought will still give new buyers “pause” when they go to sell.”

Jennie Flanigan, VANGUARD PROPERTIES

FIELD INSIGHT: Sellers aren’t losing buyers because demand is weak, but because buyers are far less forgiving than they used to be.

What surprised you most in a transaction this year?

Agents reflected on unexpected outcomes and dynamics they experienced inside transactions during 2025.

Many agents said the biggest surprise was not the overall market, but how unpredictable individual transactions became. Deals often behaved in unexpected ways. Some homes that were expected to perform modestly sold far above expectations, even during slower periods. Others that appeared well positioned stalled for weeks or months before activity returned suddenly. Appraisals were a frequent positive surprise. Despite many homes selling above asking price, most agents reported that values were confirmed during the lending process, allowing deals to move forward without disruption. Insurance emerged as a new and unexpected challenge inside active transactions. Several agents described coverage delays, premium shock or buyers backing away after receiving insurance quotes, particularly for homes in higher fire-risk areas or with older systems. Buyer behavior also stood out. Agents were surprised by how quickly buyers shifted, either disengaging suddenly or committing with little hesitation. Sellers were part of the surprise as well. Some became inflexible during escrow, misjudging their leverage once a deal was underway. Many agents described transactions that nearly fell apart but ultimately closed after renegotiation or restructuring. Others felt deals were more fragile overall. Taken together, the surprise was less about market conditions and more about how momentum, confidence and emotions shaped outcomes at the deal level.

38% — Unpredictable transaction outcomes

Deals either exceeded expectations or stalled abruptly.

29% — Sudden shifts in buyer behavior

Buyers changed direction or commitment levels quickly.

24% — Appraisals holding stronger than expected

Valuations often supported contract prices despite volatility.

17% — Unexpected transaction complexity

Title, ownership, or logistical issues created friction.

“I was able to keep inspection contingencies again for some buyers. Having that extra time in escrow for them to consider and negotiate feels like a luxury we haven’t had in years.”

Laura Arechiga, THE GRUBB CO.

“The number of offers I got on a $5M property in this market. The wealthy are always wealthy.”

Remy Weinstein, KELLER WILLIAMS

“How some sellers were willing to take a financial lose just to sell their house and move on.”

Cheryl Berger, COMPASS REAL ESTATE

“Sellers who took a lesser cash offer…offer because they were convinced the central banking system would collapse. Lots of anxiety and fear this year.”

David Gunderman, KELLER WILLIAMS

FIELD INSIGHT: The biggest surprises weren’t driven by the market, but by how much individual execution and emotional discipline shaped outcomes.

What advice would you give to 2026 buyers?

Agents shared practical guidance for how buyers should approach strategy and mindset heading into 2026.

Agents consistently advised 2026 buyers to stop trying to time the market and focus instead on what makes sense for their own lives. Waiting for perfect conditions was widely discouraged. Many agents said hesitation often leads to missed homes rather than better opportunities. Preparation came up repeatedly. Buyers who understand their finances, work with experienced professionals and are ready to act tend to have more success when the right home appears. Agents also emphasized that interest rates should not be the sole driver of decisions. While rates can change or be refinanced, missed homes and lost equity cannot be recovered. Flexibility was another strong theme. Several agents encouraged buyers to broaden their search, reconsider ideal neighborhoods or remain open to homes that are not perfectly turnkey. Those willing to adjust expectations often found better options. Persistence mattered as well. Agents noted that many successful buyers lost multiple offers before securing a home. Staying steady, learning from each attempt and continuing to engage proved more effective than stepping away.

There was some variation in advice around aggressiveness. Some agents favored decisive early offers, while others stressed selectivity and walking away when terms did not feel right. Across responses, the common thread was that 2026 will reward informed, flexible and prepared buyers rather than passive ones.

46% — Buy based on personal timing, not market timing

Agents urge buyers to prioritize life readiness over predictions.

38% — Don’t wait for perfect conditions

Hesitation often leads to missed opportunities rather than savings.

31% — Preparation and decisiveness matter most

Financial readiness and strong teams enable success.

22% — Rates are important, but not decisive

Refinancing is flexible; missed equity growth is not.

“When I look at two of the best buyer deals in 2025, my clients acted swiftly and made offers quickly after understanding the property condition, disclosures, and comparable sold data.”

Deidre Joyner, RED OAK REALTY

“Focus on the houses that don’t have fancy wallpaper. Think outside the box.”

Anna Bellomo, DISTRICT HOMES

“Seize the moment. If a house makes sense today, you will be happy tomorrow.”

Andrew Pitarre, COMPASS REAL ESTATE

“This is shelter. It isn’t an investment until you sell and find out if it appreciated or depreciated.”

Matt Heafey, COMPASS REAL ESTATE

FIELD INSIGHT: The buyers most likely to succeed in 2026 will be prepared, flexible, and focused on their own timing, not the market’s mood.

What creative strategy helped a buyer win in 2025?

Agents shared tactics and strategies that helped buyers stand out and secure homes in competitive situations.

In 2025, buyers won less with “creative” strategies and more with solid execution. Winning buyers focused on making the transaction easy and certain for the seller. Understanding what mattered most, such as timing, simplicity or flexibility, often mattered more than offering the highest price. Clean offers played a major role. Fewer contingencies, clear timelines and strong communication reduced friction and built confidence. Financing strength was another key factor. Buyers who were fully prepared, clearly qualified and backed by proactive lenders stood out (even when competing against cash offers). Relationships also mattered. Several agents cited off-market opportunities or early access that came through agent-to-agent trust in competitive neighborhoods. Some buyers used cash or short-term financing to strengthen offers, while others relied on strong pre-approval and proof of funds to achieve the same result. What happened after acceptance mattered too. Buyers who stayed flexible during inspections, solved problems quickly and avoided aggressive renegotiation were more likely to close successfully. There was variation in approach. Some agents favored aggressive terms to win early, while others emphasized discipline and walking away when deals felt forced. Across responses, the common thread was that thoughtful preparation, clarity and follow-through consistently outperformed novelty.

41% — Seller priority alignment over price

Winning offers focused on timing, certainty, and ease.

34% — Off-market or relationship-driven access

Agent relationships unlocked opportunities before broad exposure.

27% — Stronger offer structure, not more offers

Buyers succeeded by writing fewer but more competitive offers.

19% — Cash or cash-like financing strategies

Cash, delayed financing, or simplified terms increased certainty.

“Offering to pay both sides of the commission. This lowers the tax base for the Buyers and can also lower the capital gains tax for the Sellers.”

Julie Gardner, COMPASS REAL ESTATE

“Looking for listings that weren’t marketed well, or were listed with out of area agents – often, they’ll take the first offer that comes along.”

Rachel Melby, RED OAK REALTY

“This wasn’t “creative” as much as psychological: we anchored our client to real comps, made it clear she likely had one clean shot and had her choose the number she’d regret not offering. She went in at that level and won (out of 21 offers) without even getting countered.”

Daniella Brower, VANGUARD PROPERTIES

FIELD INSIGHT: The most effective “creative” strategies weren’t clever, they were clear, prepared, and seller-focused.

How did you help buyers overcome affordability concerns?

Agents explained the steps they took to help buyers bridge the gap between rising costs and purchasing power.

Many agents described affordability as more than a numbers problem. While price and monthly payment mattered, many buyers struggled just as much with fear, uncertainty and confidence. A large part of the work involved helping buyers move past anxiety and make decisions grounded in clarity rather than emotion. Reframing expectations was central. Agents often reminded buyers that a first purchase did not need to be a forever home. Instead, it could be a starting point that supported long-term goals. Education played a key role, with agents walking buyers through trade-offs around location, condition and timing to find options that aligned with their priorities. Strong lender partnerships were frequently cited as essential. Buyers benefited from working with lenders who could clearly explain options and help plan beyond the initial purchase. Many agents described affordability as a sequence rather than a single leap, encouraging buyers to think about future income growth, refinancing opportunities or eventual moves. Long, candid conversations about career trajectory and stability helped buyers regain perspective. On the tactical side, some agents reduced affordability pressure by targeting homes with less competition or focusing on listings that had already been on the market. Across responses, agents acted as translators, helping buyers turn uncertainty into informed, manageable decisions.

44% — Education and expectation-setting

Helping buyers understand trade-offs and long-term strategy.

36% — Creative or flexible financing options

Leveraging lender expertise to expand affordability.

29% — Reframing the first purchase

Positioning the home as a stepping stone, not an endpoint.

21% — Emotional reassurance and trust-building

Addressing fear and uncertainty alongside financial concerns.

“I ensured my clients connected with lenders who could offer tailored and creative financing solutions to meet their unique needs.”

Alex Morisseau, RED OAK REALTY

“Long conversations and actually listening to buyer’s concerns and not just trying to brush them off.”

Jen Wolan, DISTRICT HOMES

“We connected our buyers (especially first-time buyers) with a financial advisor. Money decision are often rooted in ingrained mindsets (scarcity vs abundance). It is helpful for a buyer to have a third party, who has no skin in the game, as a sounding board.”

Jessica Waggoner, DISTRICT HOMES

“Researching and understanding a property (and its needs deeply), which led to buyers offering a higher price, but with confidence.”

Emma Morris, RED OAK REALTY

FIELD INSIGHT: Affordability wasn’t solved by discounts, but by education, reframing, and helping buyers make confident long-term decisions.

What trend are other agents missing right now?

Agents identified shifts and signals they believe are underappreciated or overlooked by peers in the current market.

A large percentage of agents believe others are missing how fragmented the market has become. Rather than a single trend, multiple realities are playing out at the same time. Well prepared, well presented homes continue to attract strong interest, while others struggle. Agents emphasized that preparation, presentation and positioning now matter more than price tier alone, creating a sharper divide between homes that move and those that stall. Several agents also noted that buyer readiness is being underestimated. Even when activity appears quiet, buyers are paying attention and moving quickly when the right opportunity appears. This has led to renewed interest in listings that initially sat, as buyers re-engaged went pricing or competition moved in their favor. Another theme was the tendency to overfocus on interest rates while missing shifts in buyer psychology and momentum. Some agents pointed to the growing influence of AI and tech-driven wealth in the Bay Area, suggesting demand may be building in ways not yet reflected in the sales data. Others looked inward, noting that many agents still underuse social media and newer marketing channels. Video, digital storytelling and consistent online presence were cited as increasingly important tools for selling homes and building visibility. There was some disagreement on how durable current momentum is. Some see confidence building quietly, while others believe conditions remain uneven and fragile.

39% — Market segmentation being underestimated

Multiple markets are operating simultaneously by price and condition.

31% — Absorption and momentum overlooked

Rates dominate attention while real-time demand signals are missed.

24% — Buyer and seller cohort shifts

Tech-driven buyers and senior sellers are shaping activity.

18% — Underutilization of modern communication tools

“Everyone’s watching rates. Almost no one’s watching absorption. And that’s the real story.”

Kenny Truong, EXP REALTY

“Condos have lost so much value in some areas, while rents have remained high. Mortgage payments are almost equivalent to median rents in many cases. If you want to own an investment property, look into condos.”

Ellie Ridge, DISTRICT HOMES

“We had a bull run for 13 yrs , some agents have never sold in a down market. Gravy train ending. You have to actually work at your craft.”

Herman Chan, SOTHEYBY’S INT. REALTY

“Buyers in AI and tech seem to be the most capable. But seniors remain the most important (and wealthy) buyers and sellers that drive the market.”

Anja Plowright, THE GRUBB CO.

FIELD INSIGHT: The agents pulling ahead aren’t predicting the market, they’re paying attention to quieter signals others ignore.

Bold prediction: What’s one thing you think will happen in 2026?

Agents shared forward-looking expectations for rates, pricing, inventory, and buyer and seller behavior in 2026.

Agents’ predictions for 2026 point to cautious optimism rather than extreme outcomes. Many expect interest rates to ease modestly, not return to past lows, but enough to bring more buyers and sellers back into the market. Several believe this shift will weaken the lock-in effect, encouraging more move-up sellers to list. At the same time, agents warned that any easing could quickly reignite competition in specific segments. Buyers waiting for clearly “better conditions” may be surprised by how fast bidding returns for well located, well prepared homes. Increased listing activity is widely expected, particularly in the spring. However, many agents do not believe this will meaningfully ease competition. Inventory is expected to rise unevenly, varying by neighborhood and price range, rather than delivering broad relief. Price expectations are measured. Most agents do not foresee dramatic swings, but anticipate continued pressure in high demand areas. Others believe overall transaction volume will grow faster than prices, bringing more movement without a surge in values. There was real variation across responses. Some agents expect price growth to slow as volume increases. Others expect prices to push higher where demand remains strong.

47% — Gradual interest rate relief

Rates ease enough to change behavior, not enough to reset the market.

39% — Increased listings and transaction activity

More sellers re-enter as conditions feel less restrictive.

33% — Continued price appreciation

Prices rise selectively rather than uniformly.

21% — Competition returning quickly in core segments

Buyer demand rebounds faster than inventory in desirable areas.

“Interest rates will come down, but not to the levels we’ve seen in the past, and buyers will likely remain cautious.”

Negar Souza, RED OAK REALTY

“The growth of AI-driven businesses will keep Bay Area markets both stable and competitive, supporting continued demand and activity…”

Sarah Abel, COMPASS REAL ESTATE

“We have a strong sense that if 2026 is at all like 2025 it will continue to be a strong seller’s market for the properly presented and well-priced listings.”

Brenda Schaefer & Karen Starr, THE GRUBB CO.

“There will be more Baby Boomers finally making moves.”

Mindy & Talley Scott, COMPASS REAL ESTATE

FIELD INSIGHT: Most agents aren’t predicting a reset in 2026, but a release of pent-up demand that reintroduces competition faster than many expect.

Describe the East Bay market in 3 words

A market defined by contrast, intensity and local nuance.

Agents used words that signaled strength paired with tension, rather than extremes. Terms like resilient, competitive and active appeared often, but were frequently paired with words that suggested friction, selectivity or pressure. Very few agents described the market as booming or soft. The three-word exercise reinforced how difficult it is to describe the Inner East Bay with a single label. Several agents highlighted speed and responsiveness. Words implied a market that can shift quickly, where momentum builds or fades faster than expected. Others framed the East Bay as operating somewhat independently from national trends, shaped more by local demand and supply than headlines. Taken together, the three-word descriptions point to a market that remains durable, but less forgiving. Success depends on preparation, timing and local understanding rather than broad assumptions.

“Two Different Markets”

Kyle Tannahill, THE AGENCY

“Dynamic. Opportunistic. Zesty.”

Jason Mitchell, COMPASS REAL ESTATE

“Rough for Condos.”

Anna Bahnson, COMPASS REAL ESTATE

“Strong, Active, Unpredictable.”

Tracy Zhou, SOTHEBY’S INT. REALTY

“Our Own Bubble”

Jenny Wang, SOTHEBY’S INT. REALTY

“Survival of Fittest!”

Jodi Nishimura, KAI REAL ESTATE

“Making a comeback.”

Sari Cooper, RED OAK REALTY

“Dichotomy, Dynamic, Difficult.’

Hans Struzyna, KELLER WILLIAMS

FIELD INSIGHT: There was no “average” market in 2025. Success depended on reading the room correctly.

Which city or neighborhood shifted the most in 2025?

Across responses, Oakland was cited most often as the city that shifted the most in 2025. Many agents described softer demand, especially below $1M, with longer time on market and more cautious buyers. Several pointed to concerns around local conditions and services, as well as buyers choosing to stretch into nearby cities instead.

This shift was not uniform. Certain Oakland neighborhoods and well prepared homes still performed well, reinforcing how block by block outcomes had become. In contrast, Berkeley and Albany were frequently described as highly competitive, with strong demand and limited supply continuing to drive multiple offers. A smaller number of agents also noted positive momentum in El Cerrito and continued strength in Piedmont at higher price points.

There was disagreement on what the Oakland shift means going forward. Some agents see it as temporary and cyclical, while others believe it reflects a longer reset. Overall, agents agreed that 2025 made micro-location, pricing and preparation impossible to ignore.

“In Contra Costa County, the further east one goes, the more stagnant the market.”

Kelly Crawford, VANGUARD PROPERTIES

“Berkeley and Piedmont saw prices rise as the level of competition went way up.”

Tiffany Lefour, THE GRUBB CO.

“Oakland had a serious negative downturn except for Rockridge/Temescal”

Jeff Rosenbloom, RED OAK REALTY

“Piedmont prices went up for the high end. Often over $3M for homes with 1,000 sf”

Liz Behrens, THE GRUBB CO.

“Crocker Highlands in Oakland was much stronger than 2024”

Corey Weinstein, VANGUARD PROPERTIES

“The biggest shift in the East Bay market during 2025 was a very sluggish fall/early winter market specifically in Oakland, San Leandro and multi-family properties.”

Paul Talbot, COMPASS REAL ESTATE

“The mid-range home in Oakland (around $1.5M) became the market where you found some real bargains.”

Regina Jacobs, THE GRUBB CO.

“Oakland – decline. Berkeley – uptick.”

Linnette Edwards, ABIO PROPERTIES

“Oakland used to be the next step for folks moving from SF. In 2025, the SF market heated up and people were either choosing to buy within SF or cities neighboring Oakland.”

Amanda Brunato, COMPASS REAL ESTATE

“The Bushrod neighborhood (Oakland), which was so hot for so long, did not perform well this year. It was likely a victim of the city of Oakland’s public troubles.”

Tracy Davis, RED OAK REALTY

“As Oakland declined, more buyers considered El Cerrito.”

Gretchen Roethle, SALT & PINE REAL ESTATE

FIELD INSIGHT: 2025 wasn’t defined by a single city rising or falling, but by Oakland becoming the clearest example of a market sorting itself, where neighborhood, condition, and pricing precision mattered more than ever.

This page interprets agent insight through the lens of buyer behavior in 2025.

Taken together, agent responses show that buyers in 2025 were caught between a desire for certainty and a market that rarely provided it. Many entered the process looking for confirmation around timing, pricing or leverage before feeling ready to act. In reality, clarity usually followed action, not the other way around. Buyers who waited for conditions to feel settled often stalled, while those who accepted uncertainty as part of the process were better positioned to move when the right home appeared.

Success rarely came from clever tactics. It came from preparation, realistic expectations and a clear understanding of trade-offs. Buyers who spent time understanding neighborhoods, price ranges and competition moved forward with more confidence and fewer surprises. Those who recognized that list price was a starting point rather than a promise were better equipped to navigate offers and outcomes.

Local context consistently outweighed national headlines. Buyers who recalibrated expectations at the neighborhood level, stayed flexible and aligned their offers with seller priorities experienced less friction and more consistent progress through the process.

HOW THE BUYERS NAVIGATED 2025

Certainty mattered more than timing.

Buyers who waited for conditions to feel clear often stalled, while those prepared for uncertainty were able to act when the right opportunity appeared.

List price was rarely the full story.

Pricing functioned as a starting point, particularly in competitive segments, rather than a direct signal of value.

Successful approaches were simple, not clever.

Preparation, alignment with seller priorities, and strong execution mattered more than novelty.

Local context outweighed national narratives.

Buyers relying on headlines often misread leverage and competition at the neighborhood level.

Confidence followed understanding, not the other way around.

Buyers who invested time in understanding trade-offs moved forward with less hesitation.

“Buyer’s don’t always realize how unlikely it is to get a below-market price on a property listed on the open market. Most properties sell for what they should.”

Devin Ratoosh, RED OAK REALTY

“It’s defeating and disappointing for buyers to write offer after offer and not get into contract. A better strategy is to wait for the right home and write an aggressive strong offer without holding back.”

Joanna Hirsch, VANGUARD PROPERTIES

“Spend your money doing your own remodeling and repairs instead of paying for someone else’s.”

Sarah Ridge, DISTRICT HOMES

FIELD INSIGHT: Buyer outcomes in 2025 were shaped less by finding certainty and more by learning how to act thoughtfully in its absence.

This page interprets agent insight through the lens of seller outcomes in 2025.

Across markets in 2025, seller outcomes separated quickly. Demand did not disappear, but it concentrated around the right homes. Listings that were well prepared, clearly positioned and aligned with buyer expectations often generated strong early interest. Others stalled, even when pricing looked similar on paper. Condition, presentation and initial strategy mattered more than sellers expected.

Time on market carried real consequences. The first few weeks shaped how buyers perceived value and leverage. Homes that missed their early window rarely reset without adjustment. Sellers who assumed patience alone would produce a better outcome were often surprised by how quickly leverage shifted once momentum faded.

Past market peaks distorted expectations. Many sellers anchored to earlier cycles and underestimated how selective buyers had become, particularly around inspections, insurance exposure and deferred maintenance. Buyers were more willing to walk away, even after engaging seriously.

Responsiveness emerged as a key differentiator. Sellers who adjusted early, addressed feedback and stayed flexible during negotiations tended to preserve leverage. Those who resisted change often faced longer timelines and tougher renegotiations later.

The common thread was clarity. In 2025, sellers were rewarded for realism, preparation and timely decisions.

WHAT SHAPED SELLER OUTCOMES

Demand concentrated around the right homes.

Strong activity persisted for listings that aligned with buyer expectations, even as others struggled.

Condition functioned as a pricing signal.

Deferred maintenance and presentation issues were priced in quickly by buyers.

Time on market was not neutral.

Momentum in the first weeks often influenced leverage later in the process.

Past peaks distorted expectations.

Sellers anchored to earlier cycles frequently misread current buyer selectivity.

Responsiveness mattered more than patience.

Listings that adjusted early tended to perform better than those waiting for conditions to change.

“Sellers need to understand they can’t see their homes objectively. Improvements they’ve made over the years don’t automatically increase the home’s value or guarantee they’ll recoup that money when they sell.”

Lisa Chan Carnazzo, THE GRUBB CO.

“With increased competition among sellers, confidence may be lower, but this is exactly when thoughtful preparation matters most. Homes need to be positioned to shine and stand apart.”

Alex Michas, COMPASS REAL ESTATE

“Some sellers don’t seem to grasp that buyers could afford huge sums when rates were 3%, and now that rates have more than doubled, those big loans are astronomically unaffordable for the average buyer.”

Andrea Ruport, COMPASS REAL ESTATE

FIELD INSIGHT: In 2025, seller outcomes were shaped less by shifts in demand and more by how closely a home aligned with buyer expectations.

Across every section of this report, one pattern held steady: the Inner East Bay market did not behave in uniform or predictable ways.

What worked in Berkeley didn’t necessarily work in Oakland. What sold in the $1.2M range stalled at $800K. Assumptions from 2022 failed in 2025. Outcomes were shaped less by interest rate headlines and more by specifics: location, timing, preparation and expectations.

Agent experiences didn’t line up neatly across the board. In some areas, agreement was strong. In others, opinions split. Those splits weren’t contradictions. They reflected the reality that the market functioned differently depending on where you worked and what you sold.

The value of this report isn’t in any single statistic. It’s in the patterns that held and the assumptions that didn’t. Buyers and sellers who treated the Inner East Bay as a single market struggled. Those who understood it as nine distinct cities with dozens of micro-markets made better decisions.

This report is not meant to settle the conversation. It is meant to sharpen it. As a reference point, it offers a clearer way to think about a market that continues to reward nuance and punish oversimplification.

We’ll continue tracking what’s happening across brokerages and neighborhoods. For now, this is what the top inner East Bay agents saw, said and did in 2025.

“Thank you to the agents who shared what actually happened in the field. This work continues. We’re listening.”

This report would not have been possible without the participation of the contributing agents listed below. Each agent voluntarily shared time, perspective and first-hand experience drawn from active work in the Inner East Bay market. Their responses reflect direct involvement in a wide range of transactions across neighborhoods, price points and property types.

The agents included here were identified among the top 100 by closed sales volume in the defined geography and those listed represent the 66 agents who chose to participate in the survey. Collectively, they span 11 different brokerages – offering perspectives shaped by varied firm cultures, client bases and market exposures.

Their willingness to contribute thoughtful, candid responses made it possible to capture a more accurate and nuanced picture of how the market functioned during the period studied. We are grateful for their participation and for the role they played in informing this report.

Andrew Pitarre, Adrienne Krumins, Anian Tunney, Alex Michas, Alex Morisseau, Alissa Custer, Allie Pembleton, Amanda Brunato, Amy Loughran, Andrea Gordon, Andrea Ruport, Anja Plowright, Anna Bahnson, Anna Bellomo, Cheryl Berger, Claudia Mills, Corey Weinstein, Daniella Brower, David Gunderman, Deidre Joyner, Devin Ratoosh, Ellie Ridge, Emma Morris, Gillian Leslie, Gretchen Roethle, Hans Struzyna, Herman Chan, Jane Strauch, Jason Mitchell, Jeff Rosenbloom, Jen Wolan, Jennie Flanigan, Jenny Wang, Jessica Waggoner, Joanna Hirsch, Jodi Nishimura, Julie Gardner, Kara Thacker, Karen Starr, Brenda Schaefer, Kelly Crawford, Kenny Truong, Kyle Tannahill, Laura Arechiga, Linnette Edwards, Lisa Chan Carnazzo, Liz Behrens, Martha Hill, Matt Heafey, Negar Souza, Norah Brower, Pamela Strike Fullerton, Paul Talbot, Rachel Melby, Regina Jacobs, Remy Weinstein, Rosie Nysaether, Roxanna Ahlbach, Sarah Abel, Sarah Ridge, Sari Cooper, Sheri Madden, Talley Scott, Mindy Scott, Teresa Baum, Tiffany Lefour, Tracy Davis, Tracy Zhou

Design, Layout & Visual Storytelling: Laura Avalos & Tiffany Tiwater

CMG Mortgage, Inc. dba LaSalle Mortgage Services, NMLS ID# 1820 (www.nmlsconsumeraccess.org, Equal Housing Opportunity. Licensed by the Department of Financial Protection and Innovation (DFPI) under the California Residential Mortgage Lending Act No. 4150025. www.cmgfi.com/corporate/licensing 4200-2 Broadway, Oakland, CA 94611, Branch NMLS # 2682144.

Who is this report for?

This report is designed for buyers, sellers, real estate professionals and industry observers who want a grounded, on-the-ground view of the Inner East Bay housing market based on real transactions, not headlines.

How was the data collected?

The findings are based on confidential survey responses from 66 top-producing real estate agents actively working across the Inner East Bay. Responses were aggregated and analyzed to identify recurring patterns, themes and market behavior.

Which areas are included in the Inner East Bay?

The report reflects agent activity across the Inner East Bay corridor, including Alameda, Albany, Berkeley, El Cerrito, Kensington, Oakland, Piedmont, Richmond and San Leandro.

Is this an official market forecast?

No. This report is descriptive, not predictive. It captures what agents experienced in 2025 and how they are thinking about 2026 based on real-time market conditions.

Can I share or reference this report?

Yes. You’re welcome to share the report and reference its insights. If quoting or citing specific findings publicly, attribution to The Field Report: Inner East Bay is appreciated.